ML-Lecture4.2

Loading Data from Before

%load_ext autoreload

%autoreload 2

Libraries

%matplotlib inline

import sys

# or wherever you have saved the repo

sys.path.append('/Users/tlee010/Desktop/github_repos/fastai/')

from fastai.imports import *

from fastai.structured import *

from pandas_summary import DataFrameSummary

from sklearn.ensemble import RandomForestRegressor, RandomForestClassifier

from IPython.display import display

from sklearn import metrics

Load the feather file from before

import feather

df_raw = feather.read_dataframe('/Users/tlee010/kaggle/bulldozers/bulldozers-raw')

print('import complete')

import complete

Prep the data with splits and functions for the bulldozers

df_trn, y_trn, nas = proc_df(df_raw, 'SalePrice')

def split_vals(a,n): return a[:n], a[n:]

n_valid = 12000

n_trn = len(df_trn)-n_valid

X_train, X_valid = split_vals(df_trn, n_trn)

y_train, y_valid = split_vals(y_trn, n_trn)

raw_train, raw_valid = split_vals(df_raw, n_trn)

def rmse(x,y): return math.sqrt(((x-y)**2).mean())

def print_score(m):

res = [rmse(m.predict(X_train), y_train), rmse(m.predict(X_valid), y_valid),

m.score(X_train, y_train), m.score(X_valid, y_valid)]

if hasattr(m, 'oob_score_'): res.append(m.oob_score_)

print(res)

Today’s Goals

Validation Sets

Test Sets

Finalizing Random Forest Intepretation

Building your own Random Forest from scratch

Exams : All coding - random forests

What should I be able to do at this point? Week4

-

Replicate everything you’ve seen on a different dataset. We’ve seen the

bulldozerdataset. It contains rows and columns. Unstructured would be images / audio etc. -

Lesson 1 : Here is how we can create a random forest. Training validation. Score and OOB score. Here’s how we reduce overfitting. Here’s how we do it with min samples leaf / and number of trees. And get a reasonably good score

- What’s important?

- Feature important?

- How confident are you of the different predictions

- Which features should we remove

- What is the relationship between some independent variable, and other dependable variabl, all other things being equal.

Note - there’s always something to deal with (too large), super high cardinality variables, time dependence. There’s always some twist in the dataset to deal with. What’s driving the outcome, and how is it being driven.

Complex Technical Concepts

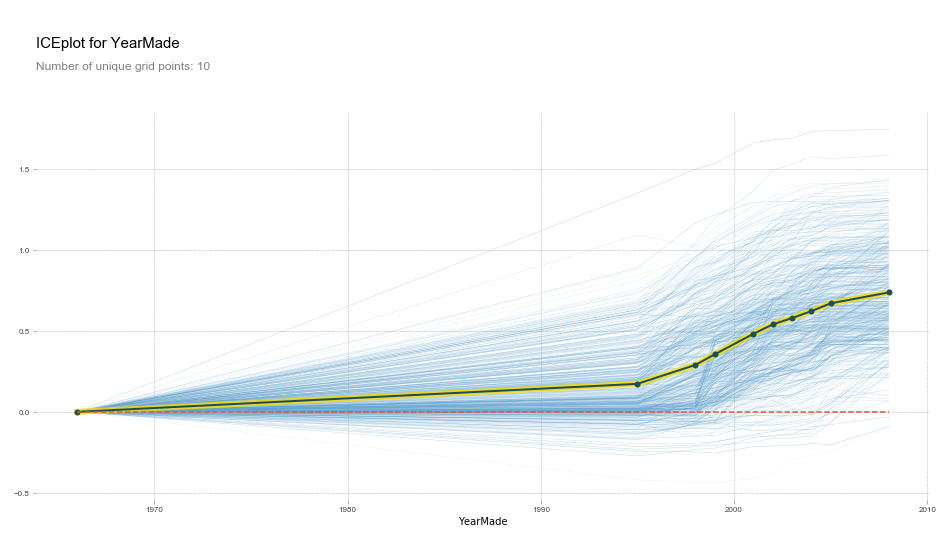

Talking about the ‘ICE Year Made Plot’

This tells you that there is basically an linear relationship. Changes the year for all values and makes a prediction. What if all things being the same, this was built a different year. The model is NOT being retrained. We are using the model and then re-running the prediction.

This plot is only looking for a subsample of 500 different years (after year 1930), for computational reasons.

y = log( change in sales price vs. if the product was made after 1960)

Outlier Handling?

Outlier in Dependent If there’s a outlier in the dependent variable, the average will be heavily affected. Leaf nodes will then have incorrect averages ( won’t change the splits too much). Tree won’t look that different, but the predictions will be different.

Outlier in Independent Not going to change anything, forests are pretty resilient.

from pdpbox import pdp

from plotnine import *

set_rf_samples(50000)

df_trn2, y_trn, nas = proc_df(df_raw, 'SalePrice', max_n_cat=7)

X_train, X_valid = split_vals(df_trn2, n_trn)

m = RandomForestRegressor(n_estimators=40, min_samples_leaf=3, max_features=0.6, n_jobs=-1)

m.fit(X_train, y_train);

x_all = get_sample(df_raw[df_raw.YearMade>1930], 500)

x = get_sample(X_train[X_train.YearMade>1930], 500)

def plot_pdp(feat, clusters=None, feat_name=None):

feat_name = feat_name or feat

p = pdp.pdp_isolate(m, x, feat)

return pdp.pdp_plot(p, feat_name, plot_lines=True,

cluster=clusters is not None, n_cluster_centers=clusters)

plot_pdp('YearMade')

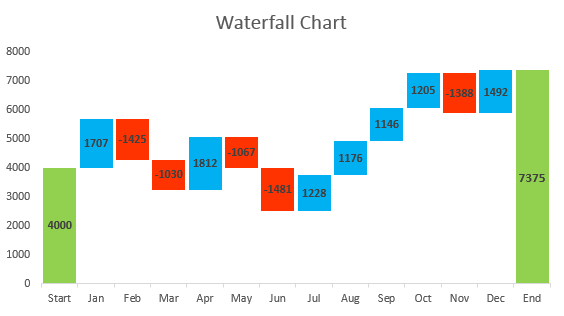

Tree Interpretation

Tree Interpreter

Looking at the affects of the different pieces

- All - 10.189

- Coupler <=0.5 - 0.156

- Enclosure <=2 -0.395 - 0.395

- ModelID <= 4573 - 0.276

- Total - 10.226

Waterfall chart - make one with the changes

Bias - is the mean of the first value

Data prep - consolidated from Lesson2-rf

df_trn, y_trn, nas = proc_df(df_raw, 'SalePrice')

def split_vals(a,n): return a[:n], a[n:]

n_valid = 12000

n_trn = len(df_trn)-n_valid

X_train, X_valid = split_vals(df_trn, n_trn)

y_train, y_valid = split_vals(y_trn, n_trn)

raw_train, raw_valid = split_vals(df_raw, n_trn)

def rmse(x,y): return math.sqrt(((x-y)**2).mean())

def print_score(m):

res = [rmse(m.predict(X_train), y_train), rmse(m.predict(X_valid), y_valid),

m.score(X_train, y_train), m.score(X_valid, y_valid)]

if hasattr(m, 'oob_score_'): res.append(m.oob_score_)

print(res)

set_rf_samples(50000)

m = RandomForestRegressor(n_estimators=40, min_samples_leaf=3, max_features=0.5, n_jobs=-1, oob_score=True)

m.fit(X_train, y_train)

print_score(m)

fi = rf_feat_importance(m, df_trn); fi[:10]

[0.20546521753082297, 0.2509610106685115, 0.91177098095443698, 0.88752383935747015, 0.89480604501280936]

.dataframe tbody tr th {

vertical-align: top;

}

.dataframe thead th {

text-align: right;

}

| cols | imp | |

|---|---|---|

| 64 | age | 0.144301 |

| 13 | ProductSize | 0.109078 |

| 14 | fiProductClassDesc | 0.096000 |

| 37 | Coupler_System | 0.079007 |

| 5 | YearMade | 0.068811 |

| 39 | Hydraulics_Flow | 0.064676 |

| 2 | ModelID | 0.064318 |

| 38 | Grouser_Tracks | 0.049578 |

| 10 | fiSecondaryDesc | 0.039151 |

| 19 | Enclosure | 0.032419 |

Tracking a Row’s Prediction through tree interpreter / Contribution Editing

Bias - or the mean value

prediction, bias, contributions = ti.predict(m, row)

prediction[0], bias[0]

(9.308455935297518, 10.106152392409408)

Now we add all the tree influences

[('ProductSize', 'Mini', -0.54680742853695008),

('age', 11, -0.12507089451852943),

('fiProductClassDesc',

'Hydraulic Excavator, Track - 3.0 to 4.0 Metric Tons',

-0.11143111128570773),

Then we add in all the contributions

contributions[0].sum()

-0.7383536391949419

Final prediction

prediction[0],

9.308455935297518

Why its important - the tree interpretter. We can graphically and easily describe how we track the prediction.

When combining different trees, what if you are missing features in some? - Even if feature only appears once, the average will be that single value, divided by the number of the trees.

**What if this is classification ? ** the trees will be split by the average of the 1’s and 0s. So it would answer “how often does this occur”? We usually use cross-entropy, which is negative log likelihood. RMSE is not a bad approach.

from treeinterpreter import treeinterpreter as ti

feats=['SalesID', 'saleElapsed', 'MachineID', 'age', 'YearMade', 'saleDayofyear']

to_keep = fi[fi.imp>0.005].cols; len(to_keep)

df_keep = df_trn[to_keep].copy()

X_train, X_valid = split_vals(df_keep, n_trn)

m = RandomForestRegressor(n_estimators=40, min_samples_leaf=3, max_features=0.5, n_jobs=-1, oob_score=True)

m.fit(X_train, y_train)

df_raw.YearMade[df_raw.YearMade<1950] = 1950

df_keep['age'] = df_raw['age'] = df_raw.saleYear-df_raw.YearMade

X_train, X_valid = split_vals(df_keep, n_trn)

m = RandomForestRegressor(n_estimators=40, min_samples_leaf=3, max_features=0.6, n_jobs=-1)

m.fit(X_train, y_train)

df_train, df_valid = split_vals(df_raw[df_keep.columns], n_trn)

row = X_valid.values[None,0]; row

array([[ 11, 5, 17, 0, 1999, 0, 665, 0,

0, 1, 3232, 1111, 1284595200, 4364751, 0, 2300944,

4, 2010, 0, 4, 0, 259, 35, 16,

2, 12]])

prediction, bias, contributions = ti.predict(m, row)

prediction[0], bias[0]

(9.4120004499352454, 10.106191974635667)

idxs = np.argsort(contributions[0])

[o for o in zip(df_keep.columns[idxs], df_valid.iloc[0][idxs], contributions[0][idxs])]

[('ProductSize', 'Mini', -0.47483352839715726),

('age', 11, -0.097889119451887302),

('fiProductClassDesc',

'Hydraulic Excavator, Track - 3.0 to 4.0 Metric Tons',

-0.076471050183981107),

('fiBaseModel', 'KX121', -0.066841565760360627),

('fiSecondaryDesc', nan, -0.053024465856433965),

('fiModelDesc', 'KX1212', -0.050252781130077161),

('fiModelDescriptor', nan, -0.030473957539144125),

('Enclosure', 'EROPS', -0.030300855486490041),

('MachineID', 2300944, -0.0214149038864321),

('SalesID', 4364751, -0.018611091431251836),

('state', 'Ohio', -0.018457661613301778),

('saleElapsed', 1284595200, -0.006866623476152434),

('saleYear', 2010, -0.0054711996267921672),

('saleDayofyear', 259, -0.0031785685023805409),

('Tire_Size', nan, -0.0030972153456157335),

('Drive_System', nan, 0.0035246475564432167),

('ProductGroupDesc', 'Track Excavators', 0.0071280184890852635),

('ProductGroup', 'TEX', 0.0078641941839247224),

('saleDay', 16, 0.011294146761423107),

('Hydraulics', 'Standard', 0.013414957232583813),

('Grouser_Tracks', nan, 0.021113325822571926),

('Hydraulics_Flow', nan, 0.023690314863592389),

('ModelID', 665, 0.027764047395303849),

('Track_Type', 'Steel', 0.030322411392836646),

('Coupler_System', nan, 0.052404167060031571),

('YearMade', 1999, 0.064472832229242633)]

contributions[0].sum()

-0.69419152470041912

Validation Sets

Building a model on a training set. We make a accurate training set, but the test set says that its not good. We tune + go back to the test set, and see if it looks better. We iterate, and we find something that works really well.

Q: Does that mean we have reached generalization ?

MAYBE

So now we have 3 data sets :

- TRAIN

- VALID

- TEST (lock away) <- final word on if generalized

Creating an appropriate test set is the most important thing

-

If the test set is wrong, and does not tell you if the model is valid or not. You dont know if you are right or not.

-

It takes time to put model into production, to test and implement. And maybe by the time that it goes to market the world is a very different place.

-

The test set should also take real world into account. Lets see what it looks like for forecasting:

| Set | Duration |

|---|---|

| Test | most recent 3 months |

| Valid | the next recent 3 months |

| train | other months |

What Kaggle does for test sets

##### 30% is used for the Public Leaderboard ##### 70% is the private leaderboard (only revealed at the end) If you drop in Kaggle between the boards, that means you are probably overfitting. Ideally you should have similar scores between the two datasets.** Example ** - start-up built a new recommender based on user social graphs (with history), but during the roll out, all the users were brand new to the service without a social history so the training and the actual use was much different between the two

** Example Grocery ** - Validation sets

- Last Two Weeks

- Last Month

- Last 2 months etc.

Then plot these validation sets against the kaggle to determine how consistent the scores are

Q: We have 2 scores from the OOB and score from a random training set how would they compare?

Answer For the OOB - we take a row, was it used in tree 1, 2, 3, or 4? So we can only use a subsets of the trees. We are using a smaller subset of the overall forest. More trees = more average = smoother results. So OOB is a bit worse, since fewer number of trees.

If the R^2 is better for OOB - you aren’t overfitting, but validation score is bad, you are still generalized, but still not doing well of predicting. Could be missing a feature, or could be missing some additional features.

How is my validation set different to my training set?

Test set, is it a random set or different in some way? [IN this example, looking at the time dependence]

- combine the datasets together (test and train)

- 0 is training, 1 is test set

- Try to predict if the dataset is from the training or the test set (don’t need target’)

- Use a random forest

df_ext = df_keep.copy()

df_ext['is_valid'] = 1

df_ext.is_valid[:n_trn] = 0

x, y, _ = proc_df(df_ext, 'is_valid')

m = RandomForestClassifier(n_estimators=40, min_samples_leaf=3, max_features=0.5, n_jobs=-1, oob_score=True)

m.fit(x, y);

m.oob_score_

0.99999002804612025

fi = rf_feat_importance(m, x); fi[:10]

.dataframe tbody tr th {

vertical-align: top;

}

.dataframe thead th {

text-align: right;

}

| cols | imp | |

|---|---|---|

| 13 | SalesID | 0.812214 |

| 12 | saleElapsed | 0.140304 |

| 15 | MachineID | 0.027869 |

| 17 | saleYear | 0.007917 |

| 4 | YearMade | 0.003177 |

| 11 | fiBaseModel | 0.001311 |

| 9 | Enclosure | 0.001307 |

| 10 | fiModelDesc | 0.001139 |

| 25 | Hydraulics | 0.001096 |

| 21 | saleDayofyear | 0.000907 |

Discussion: more recent machines are given newer ids. Lets look at the first 3

feats=['SalesID', 'saleElapsed', 'MachineID']

(X_train[feats]/1000).describe()

.dataframe tbody tr th {

vertical-align: top;

}

.dataframe thead th {

text-align: right;

}

| SalesID | saleElapsed | MachineID | |

|---|---|---|---|

| count | 389125.000000 | 3.891250e+05 | 389125.000000 |

| mean | 1800.452485 | 1.084797e+06 | 1206.796148 |

| std | 595.627288 | 1.803913e+05 | 430.850552 |

| min | 1139.246000 | 6.009984e+05 | 0.000000 |

| 25% | 1413.348000 | 9.666432e+05 | 1087.016000 |

| 50% | 1632.093000 | 1.134605e+06 | 1273.859000 |

| 75% | 2210.453000 | 1.234138e+06 | 1458.661000 |

| max | 4364.741000 | 1.325117e+06 | 2313.821000 |

Confirm that these fields are time dependent

(X_valid[feats]/1000).describe()

.dataframe tbody tr th {

vertical-align: top;

}

.dataframe thead th {

text-align: right;

}

| SalesID | saleElapsed | MachineID | |

|---|---|---|---|

| count | 12000.000000 | 1.200000e+04 | 12000.000000 |

| mean | 5786.967651 | 1.306609e+06 | 1578.049709 |

| std | 836.899608 | 2.497808e+04 | 589.497173 |

| min | 4364.751000 | 1.174522e+06 | 0.830000 |

| 25% | 4408.580750 | 1.309219e+06 | 1271.225250 |

| 50% | 6272.538500 | 1.316045e+06 | 1825.317000 |

| 75% | 6291.792250 | 1.321402e+06 | 1907.858000 |

| max | 6333.342000 | 1.325203e+06 | 2486.330000 |

x.drop(feats, axis=1, inplace=True)

Retrain and examine (without SalesID, saleElapse, MachineID)

m = RandomForestClassifier(n_estimators=40, min_samples_leaf=3, max_features=0.5, n_jobs=-1, oob_score=True)

m.fit(x, y);

m.oob_score_

0.98550825802430664

fi = rf_feat_importance(m, x); fi[:10]

.dataframe tbody tr th {

vertical-align: top;

}

.dataframe thead th {

text-align: right;

}

| cols | imp | |

|---|---|---|

| 14 | saleYear | 0.323026 |

| 18 | saleDayofyear | 0.254053 |

| 6 | ModelID | 0.055675 |

| 20 | saleDay | 0.049019 |

| 10 | fiModelDesc | 0.039258 |

| 19 | state | 0.036700 |

| 4 | YearMade | 0.033622 |

| 11 | fiBaseModel | 0.029656 |

| 0 | age | 0.028444 |

| 9 | Enclosure | 0.025474 |

Lets’ make a RF, remove these features 1 at a time

set_rf_samples(50000)

Suspected time dependent features to randomly drop

feats=['SalesID', 'saleElapsed', 'MachineID', 'age', 'YearMade', 'saleDayofyear']

X_train, X_valid = split_vals(df_keep, n_trn)

m = RandomForestRegressor(n_estimators=40, min_samples_leaf=3, max_features=0.5, n_jobs=-1, oob_score=True)

m.fit(X_train, y_train)

print_score(m)

[0.1239400515957124, 0.22291901531335712, 0.96789607210517048, 0.9112553448779237, 0.90931684420931058]

Loop through and try and predict

for f in feats:

df_subs = df_keep.drop(f, axis=1)

X_train, X_valid = split_vals(df_subs, n_trn)

m = RandomForestRegressor(n_estimators=40, min_samples_leaf=3, max_features=0.5, n_jobs=-1, oob_score=True)

m.fit(X_train, y_train)

print(f)

print_score(m)

SalesID

[0.1277492887571901, 0.2204551799395666, 0.96589234920766698, 0.91320622270794161, 0.90939053874335463]

saleElapsed

[0.12710539554859768, 0.22632082290926267, 0.96623530748651576, 0.90852614098104056, 0.90801683810739509]

MachineID

[0.12716844809238703, 0.2202002816170202, 0.96620180021024593, 0.91340681493893672, 0.91102000725277199]

age

[0.12476982192438187, 0.2249066056487989, 0.96746476585288899, 0.9096657597638339, 0.90975752919803488]

YearMade

[0.12462348237415515, 0.2248658079813547, 0.9675410406974656, 0.90969852973976595, 0.90968496748530769]

saleDayofyear

[0.1277516360233823, 0.22391746049979452, 0.96589109580779475, 0.91045859717612299, 0.90856106645875168]

Discussion

We remove SalesID and MachineID and saleDay of the year because it seems like it is time dependent which we want to remove

reset_rf_samples()

Our Current Best Model

df_subs = df_keep.drop(['SalesID', 'MachineID', 'saleDayofyear'], axis=1)

X_train, X_valid = split_vals(df_subs, n_trn)

m = RandomForestRegressor(n_estimators=40, min_samples_leaf=3, max_features=0.5, n_jobs=-1, oob_score=True)

m.fit(X_train, y_train)

print_score(m)

[0.13685772048830452, 0.21666937899122155, 0.96085525842884623, 0.91616158655825652, 0.91016508458294254]

plot_fi(rf_feat_importance(m, X_train));

Our Best Model

Upping the number of trees.

m = RandomForestRegressor(n_estimators=160, max_features=0.5, n_jobs=-1, oob_score=True)

%time m.fit(X_train, y_train)

print_score(m)

CPU times: user 7min 9s, sys: 5.96 s, total: 7min 15s

Wall time: 1min 8s

[0.07483820926906463, 0.2204628379662015, 0.98829472556490661, 0.91320019263323127, 0.91431911498508012]

RandomForest from Scratch

%load_ext autoreload

%autoreload 2

The autoreload extension is already loaded. To reload it, use:

%reload_ext autoreload

How do you know if you coded some thing incorrectly?

It’s good to have a dataset to compare to. Test envir (existing library, lets replicate what it does) - we will get the same answers as sklearn. (Our golden standard)

%matplotlib inline

from fastai.imports import *

from fastai.structured import *

from sklearn.ensemble import RandomForestRegressor, RandomForestClassifier

from IPython.display import display

from sklearn import metrics

Load the Raw data

PATH = "data/bulldozers/"

%time df_raw = feather.read_dataframe('/Users/tlee010/kaggle/bulldozers/bulldozers-raw')

CPU times: user 109 ms, sys: 73.9 ms, total: 183 ms

Wall time: 290 ms

df_trn, y_trn, _ = proc_df(df_raw, 'SalePrice')

Setup normal data splits

def split_vals(a,n): return a[:n], a[n:]

n_valid = 12000

n_trn = len(df_trn)-n_valid

X_train, X_valid = split_vals(df_trn, n_trn)

y_train, y_valid = split_vals(y_trn, n_trn)

raw_train, raw_valid = split_vals(df_raw, n_trn)

Writing Trees, assuming that some other things exist

class TreeEnsemble():

## this is called when TreeEnsemble() is used

def __init__(self, x, y, n_trees, sample_sz, min_leaf=5):

np.random.seed(42)

# saving all the data to the object

# self is the actual object, all the non-self ones, are the

# user inputs

self.x, self.y, self.sample_sz, self.min_leaf = x, y, sample_sz, min_leaf

# creating n amount of trees

self.trees = [self.create_tree() for i in range(n_trees)]

def create_tree(self):

# getting random index, and limits how big it is by the sample size

rnd_idxs = np.random.permutation(len(self.y))[:self.sample_sz]

# Makes a new decision tree based on the random indexs

return DecisionTree(self.x.iloc[idxs], self.y[rnd_idxs],

idxs=np.array(range(self.sample_sz)), min_leaf=self.min_leaf)

def predict(x):

# for each tree, predict for each tree, then return the average

# using list comprehension

return np.mean([t.predict(x) for t in self.trees], axis=0)

# this basically just stores a bunch of data at the moment

class DecisionTree():

def __init__(self, x,y,idxs, min_leaf=5):

self.x, self.y, self.idxs, self.min_leaf = x, y, idxs, min_leaf

Aside on Object Oriented Programming

A good beginners reference:

https://python.swaroopch.com/oop.html

Instantiate a tree ensemble

### note when this is called, __init__ ( ... ) is already called

a = TreeEnsemble(X_train, y_train, n_trees=10, sample_sz=1000, min_leaf=3)

a.min_leaf

3

Also note: we haven’t designed predict yet. But since we haven’t called it, there’s no error

Lets make a basic Model

m = TreeEnsemble(X_train, y_train, n_trees=10, sample_sz=1000, min_leaf=3)

Lets look at our random index sample that we discussed in the create_tree method

Note that the first tree will have all the ids.

m.create_tree().idxs[:25]

array([ 0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18, 19, 20, 21, 22, 23, 24])